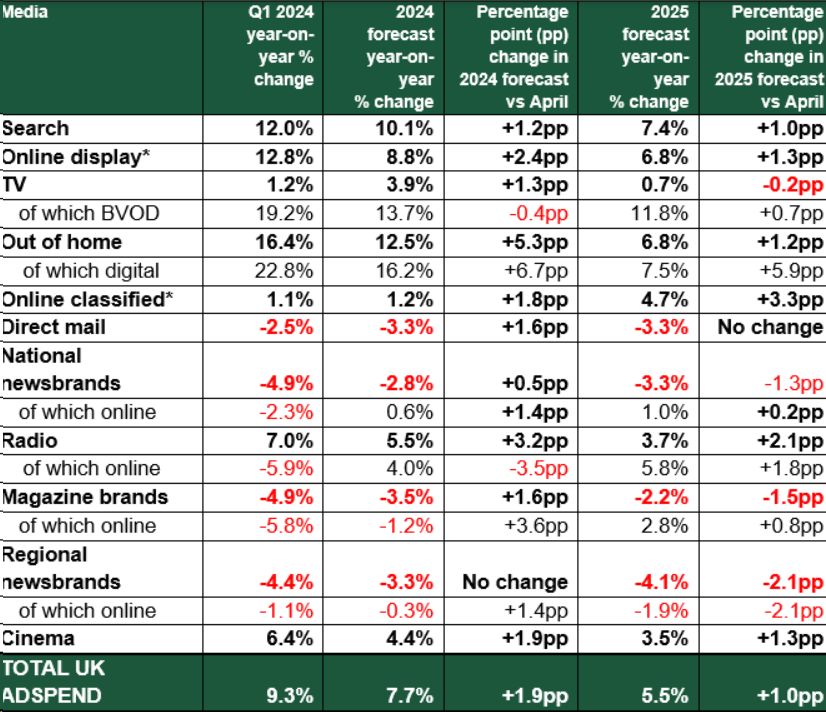

The latest report from the Advertising Association and WARC reveals that UK ad spend increased by 9.3% to reach approximately $11.6 billion during the first quarter of 2024, setting a new record for this period. This growth exceeded forecasts due to stronger-than-expected online activity, with digital formats comprising 79.7% of total UK ad spend in Q1 2024.

The updated AA/WARC projections anticipate UK ad spend to rise by 9.2% in Q2, reaching around $12.2 billion, driven by increased spending related to events such as the men’s Euros and a snap General Election. This would result in a 9.3% increase for the first half of 2024, totaling about $23.8 billion, with full-year growth expected to hit approximately $49.6 billion.

In addition to digital, sectors likely to see a boost include Out of Home (up 12.5%), Search (up 10.1%), and Radio (up 5.5%). Advertising spend on the Broadcaster Video On-Demand (BVOD) segment of TV is projected to surpass the $1.3 billion mark for the first time, reflecting a 13.7% increase, fueled by a strong summer of sports events.

A further 5.5% increase is expected in 2025, by which time the UK advertising market is set to reach around $52.4 billion.

Stephen Woodford, CEO of AA, commented: “It’s encouraging to see real growth and upgraded forecasts in the advertising market for Q1 this year, highlighting our industry’s role in driving the UK’s economic recovery. This also serves as a timely reminder of the sector’s dynamism as the new Government aims to foster growth through political stability and a fresh industrial strategy.

“Advertising is a nationwide industry, with three in five advertising jobs located outside London, and it plays a crucial role in the development of the digital economy across the country.”

James McDonald of WARC added: “The push for AI adoption in the advertising industry has intensified, with major online platforms introducing their own solutions, which have positively impacted their bottom lines. The full effects of these tools will become clearer over time, though the first quarter results were notably boosted by increased ad loads and associated performance costs online.

“However, the continued strength of traditional display media – particularly TV, out of home, radio, and cinema – was also apparent in the first quarter, and we expect this to continue into the second quarter, partly due to short-term factors such as the Men’s Euros and the snap General Election. Overall, our outlook for the year is more optimistic than our previous projection in April, with a forecasted 7.7% rise in total ad spend this year, ahead of the average rate recorded before the pandemic.”